Not Made in the U.S.A.

Posted on: September 25, 2014 by Martin Curiel, CFA in Investments

I am proud to be an American. My family came to this country from Mexico to pursue opportunities not offered to them by their homeland, and I have benefited tremendously from their effort, risk taking, and sacrifice. America is a place where an individual – through hard work, persistence, and a little luck – can achieve almost anything. It is a place where innovative companies like Apple, Google, Facebook, and General Electric were born and have changed the world in profound ways.

I express my patriotism in multiple ways, including paying my taxes on time, participating in national and local elections (most of the time), and contributing to my community (www.rfdf.org). However, when it comes to designing my investment portfolio, I do not adhere to the philosophy that America is the “best,” at least not always. When it comes to investing, my objective is to earn the highest return possible for a given level of risk; in other words, to achieve the highest risk-adjusted return. While I believe this country is the best place to live for my family, I do not believe companies headquartered in the U.S. have a monopoly on meeting my investment objectives. I also contend that there is nothing positive about investing my capital in the U.S. for reasons other than maximizing my risk-adjusted returns. As we have seen throughout the world, when capital flows to a country, sector, or company for reasons other than maximizing profits, failure is a near guarantee (see Venezuela). For me, it is irrelevant if my investment return comes from a company located in my hometown of Mountain View, California, or from one located in a Chinese city whose name is too difficult for me to pronounce or write.

In this article, I’d like to discuss the issue of home-country bias, which is an investor’s natural tendency to invest in domestic markets.In my experience, many Americans fall prey to this bias, as their portfolios are significantly, if not completely, exposed to the U.S. stock market. We live in a globalized economy, and so overweighting a certain region of the world for reasons such as comfort or patriotism poses significant risks to an investor.

Made in the U.S.A.

In a study performed by Morningstar in 2013, U.S. mutual fund investors held an average of 73% of their total stock portfolio in U.S.-based funds. Why the emphasis on investing at home? In my discussions with other investors, there are four main reasons why this seems to be the case:

- Comfort With the Known- “Invest in what you know” is a phrase I’ve heard repeated many times by my investor friends. The thesis is that if you understand the product or service, you are more likely to do a better job in terms of analyzing the investment merits of the company that creates it. This philosophy gets expressed not only at the individual stock level (e.g., we all know someone who invests in Apple because they love the iPhone) but also at the fund and allocation level. Another related issue is how investors define the “market.” For example, many people I know think the S&P 500 or the Dow Jones Industrial Average is the ultimate benchmark for their portfolios. Both of these indices only cover a small subset of the U.S. market, let alone the world market.

- Structural Issues- Millions of Americans invest through their company-sponsored 401(k)s or through an IRA account (usually rolling over old 401(k)s). One common strategy we see with such individuals is the use of target date funds. These are all-in-one funds that periodically reallocate their holdings to a more conservative mix over time as the fund holder approaches the target date – usually retirement. This category of funds works well for those individuals who don’t have the time to do research and/or the inclination to hire an advisor to do the allocation for them. Target date funds, however, tend to exhibit a very large overweight to domestic markets. For example, take Vanguard’s 2050 Fund (Symbol: VFIFX). According to Morningstar.com, as of 8/31/2014, the fund’s stock allocation has about 70% exposure to the U.S. versus a global index of about 50% – that is a very large bet in favor of the U.S. and against international stocks. In our experience, many clients don’t realize that their target date fund is making such a large bet.

- Perception of Foreign Markets- Back in my college days, when I was planning my Spring break to Mexico, many friends would advise me something like, “You shouldn’t go to Mexico. They’ll shoot you there.” Needless to say, I did party many years in Mexico without getting shot or hearing about another American getting shot. Individuals, particularly those who have not traveled extensively, often have misconceptions about foreigners and foreign markets. For example, many believe that there is widespread corruption in places like China and India, and by extension very few investment opportunities. The fact that things don’t operate as smoothly as they do in the U.S. is not necessarily a bad thing from an investor’s perspective. Factors such as extra bureaucracy and underdeveloped regulatory bodies may ultimately yield high investment returns.

- Higher Fees– Trading stocks and bonds in foreign markets is generally more expensive relative to more developed markets like the U.S. Even an international-based mutual fund or ETF will generally have a higher expense ratio than a comparable U.S. fund. We are in agreement that higher fees systematically destroy wealth, but also believe that the risk/reward benefits are much larger than the incremental fees in certain cases.

As I’ve discussed in other articles, the stock market is the most democratic forum in the world. An index that is based on a stock’s market capitalization (# of shares * price of share) will express the wishes of the millions of investors around the world (not just the U.S.). The chart below represents a common Global Index, the FTSE Global All Cap Index (using The Vanguard Total World Stock ETF as a proxy):

Source: Vanguard.com; data as of 8/31/2014.

Our belief is that the starting point of any investment program should be a global market index such as the FTSE Global All Cap Index or the All Country World Index (ACWI), which in our view is the true definition of the “market” in terms of publicly traded stocks. At the time of this writing, both indices call for about 50% exposure to international markets. Any deviation from the index should be made with a strong thesis of why a different exposure will outperform, and should be limited. For example, if an investor truly believes that U.S. management is superior at increasing return on capital and that this idea will lead to outperformance, it is reasonable to express that thesis by overweighting the U.S. markets. It’s also important, however, to measure the results of that “bet” every quarter or at least every year. If the investor has 100% exposure to the U.S. market, she is essentially making a 50% overweight in favor of the U.S., which we believe is excessive.

Aside from the active management risk inherent in going against the market, there are other compelling reasons to invest in international markets. Three come to mind:

- Diversification

- Exposure to Local Markets

- Performance Potential

Diversification

As discussed before, one goal of investing is achieving the highest risk-adjusted returns possible. One can think of this objective as maximizing the ratio of Return/Risk. Reducing the denominator of this equation, without affecting the numerator, is indeed a challenging task. One common technique is to combine assets in a portfolio that under the same conditions will behave differently (e.g., they won’t be perfectly “correlated”). The common saying is “don’t put all your eggs in one basket”; diversification is about having lots of “baskets.”

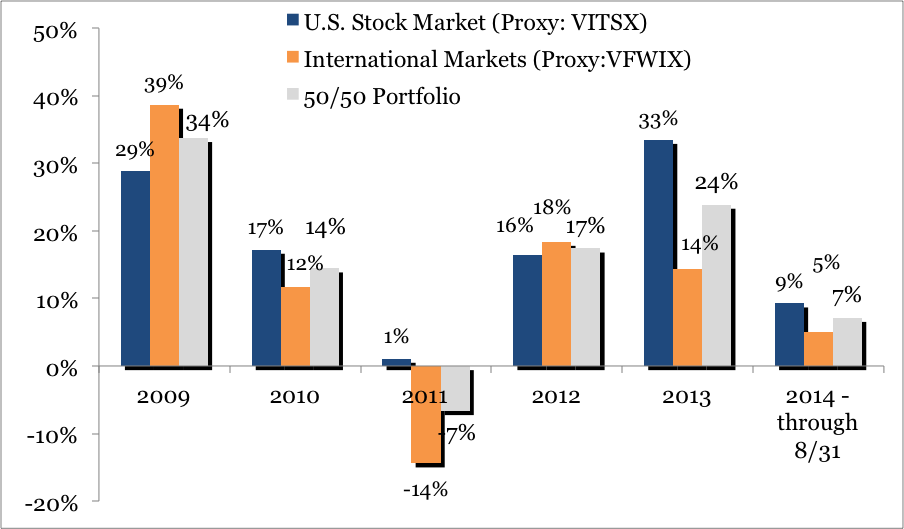

In the case of U.S. versus international stocks, the question is: Is the U.S. stock market indeed different from the international one? One way to answer this is to look at the return stream over time. Below is a chart that looks at yearly returns from 2009 through 8/31/2014:

As one can observe, over the last 5+ years, the U.S. stock market has never behaved exactly like the international markets. For example, in 2009 international markets returned nearly 8% more than the U.S. markets, and in 2013 the U.S. outperformed international markets by over 15%. The bar graph also shows the hypothetical return of a 50% U.S. and 50% international portfolio, which is a ratio close to what the world stock market indices call for. By simple observation, one can see that the 50/50 portfolio exhibited less volatility over time and helped during the time periods when the U.S. underperformed. Clearly, the U.S. and international markets are not perfectly correlated, and there is a strong case to be made for international stocks adding to the diversification objective.

Exposure to Local Markets

In March 2011, Mattel, a U.S.-based company, closed its flagship Barbie store in Shanghai, China. Mattel failed to win over the Chinese consumer – some argued the price points were too high, while others pointed to the notion that Chinese girls preferred animated characters such as Hello Kitty. A great article on the topic by Matthews Asia can be found here. A similar story can be told about companies like Home Depot, Best Buy, Facebook, and Google – all tried to wield their strong western brands in the East, only to fail miserably (at least for now). The point here is that, like in the U.S., there are numerous homegrown companies that have clearly figured out how to serve the local consumer/client much better than an outsider could. Baidu in China, Grupo Modelo in Mexico, and Copa Holdings in Panama are some of the names that come to mind. It is true that companies like Apple and General Motors derive an ever-increasing share of their revenues from offshore operations, but to get true exposure to the global economy, there is a case to be made that one needs exposure directly to foreign-owned companies.

Performance PotentialWe believe that over the long term, public markets are efficient. Over the short term, however, temporary dislocations can occur mainly due to investor behavioral factors such as overconfidence, herd mentality, and loss aversion. We believe that when markets have gone up significantly, there is tremendous risk of a downturn.

The table below shows the 2013 and 2014 (through August 31) performance of the U.S. and select international markets:

Betting on a group of securities ensures some diversification relative to single investments. It is also executable from a research perspective; we cover less than 100 of these groupings. Adequately covering every single investable security in the world would be a nearly impossible task. Having a small universe of investable products also aids with performance and risk tracking.

The historical average return of U.S. stocks has been around 8%, yet in 2013, return was more than 4x that at 33.5%. In 2013, the U.S. outperformed virtually every international market. We don’t profess to have a crystal ball about what will take place in the future and past performance is certainly not an indicator of future returns. However, we do believe that returns of 33%+ in any market are not likely to persist over the long term. One can see in the 2014 data through August 31 that the picture looks much more different compared to 2013. For example, emerging markets, which had a negative return in 2013, have done much better than the U.S. in 2014. India is another example of a market that was underperforming last year, but which this year has delivered nearly 3x the U.S. The main point here is that the U.S. has done very well – relative to international markets and much higher than historical averages – in recent periods. Will this trend continue? No one knows for sure, but such strong returns are not likely to last forever.

SummaryI pledge allegiance to the flag of the United States of America. My country is a beautiful place, and there is nowhere else I would rather call home. However, when it comes to earning the maximum risk-adjusted returns, I do believe that international markets offer tremendous opportunities. The benefits of international investing are many, including diversification, exposure to promising local markets, and the potential for outperformance. In my opinion, maximizing the returns on one’s capital is a better expression of patriotism than supporting locally owned companies exclusively. I pledge allegiance to the flag of the United States of America.

Disclosures: Non-deposit investment products are not FDIC insured, are not deposits or other obligations of MYeCFO, are not guaranteed by MYeCFO, and involve investment risks, including possible loss of principal. The information contained in this article is for informational purposes only and contains confidential and proprietary information that is subject to change without notice. Any opinions expressed are current only as of the time made and are subject to change without notice. This article may include estimates, projections, and other forward-looking statements; however, due to numerous factors, actual events may differ substantially from those presented. Any graphs and tables that make up this article have been based on unaudited, third party data and performance information provided to us by one or more commercial databases or publicly available websites and reports. While we believe this information to be reliable, MYeCFO bears no responsibility whatsoever for any errors or omissions. Additionally, please be aware that past performance is no guide to the future performance of any manager or strategy, and that the performance results displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Therefore, caution must be used inferring that these results are indicative of the future performance of any strategy. Index results assume re-investment of all dividends and interest. Moreover, the information provided is not intended to be, and should not be construed as, investment, legal, or tax advice. Nothing contained herein should be construed as a recommendation or advice to purchase or sell any security, investment, or portfolio allocation. Any investment advice provided by MYeCFO is client-specific based on each client’s risk tolerance and investment objectives. Please consult your MYeCFO Advisor directly for investment advice related to your specific investment portfolio.